When Value Keeps Moving

Support Becomes Circulation

There is a big difference between lending systems or giving out cash and growing a system where value keeps moving.

In ordinary lending, someone receives money and is expected to repay money. In many cash allocation programs, support reaches a household, helps with an immediate need, and may then leave the community. Both can be useful. But regenerative systems ask a deeper question: how can support continue circulating after the first person receives it?

In Mnarani and Kiriba, community groups are showing how this can work. Whether the starting point is weekly group savings or basic income support from FairSpirit Foundation, the pool creates a shared place where people access what they need and put in commitments to repay through cash, goods, services, or labour. These commitments become vouchers held by the group, visible to others, and usable like a curated community marketplace.

This article is written by Joyce Kamau and Njambi Njoroge, with deep appreciation to Emmanuel Kahindi, the champion supporting the Muungano group of village elders, and George Shungu, the champion supporting groups in Kiriba.

When Support Becomes Circulation

Savings, Basic Income, and Commitment Pools in Mnarani and Kiriba

In many villages, mutual support has always existed. People contribute what they can, lend to one another, work together, care for one another, and respond when a neighbour is in need. These systems are not new. What is changing is how these traditions are being strengthened through new tools that make commitments easier to see, exchange, and fulfill.

A commitment pool does not replace community trust. It gives that trust a shared place to move.

In Mnarani, the starting point is a savings and lending system led by village elders. In Kiriba, the starting point is pooled basic income support provided through FairSpirit Foundation. The source of the first seed is different, but the pattern is the same. Value enters the pool. Members access support. In return, they place their own commitments into the pool. Those commitments can then be used by others, exchanged, fulfilled, or repaid.

This is what makes the system different from normal lending or simple cash distribution. The value does not stop with the first person who receives it. It keeps moving.

Muungano: From Ledger Books to a Living Pool

By Joyce Kamau

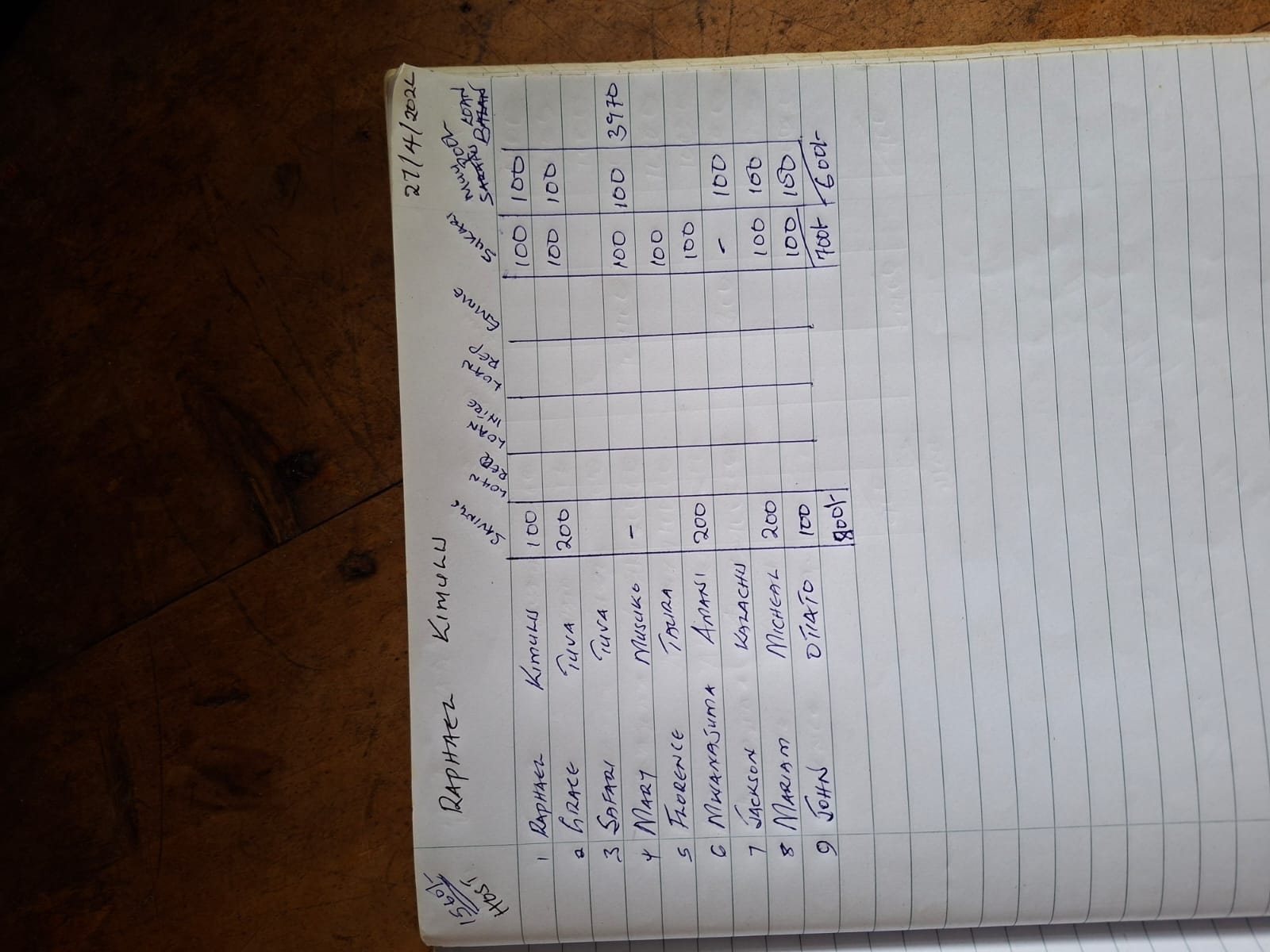

Muungano is a group of elders from Mnarani village in Kilifi. These are trusted people in the community, elders who already play an important role in keeping the village connected. The group has existed for about five years and is registered under social services.

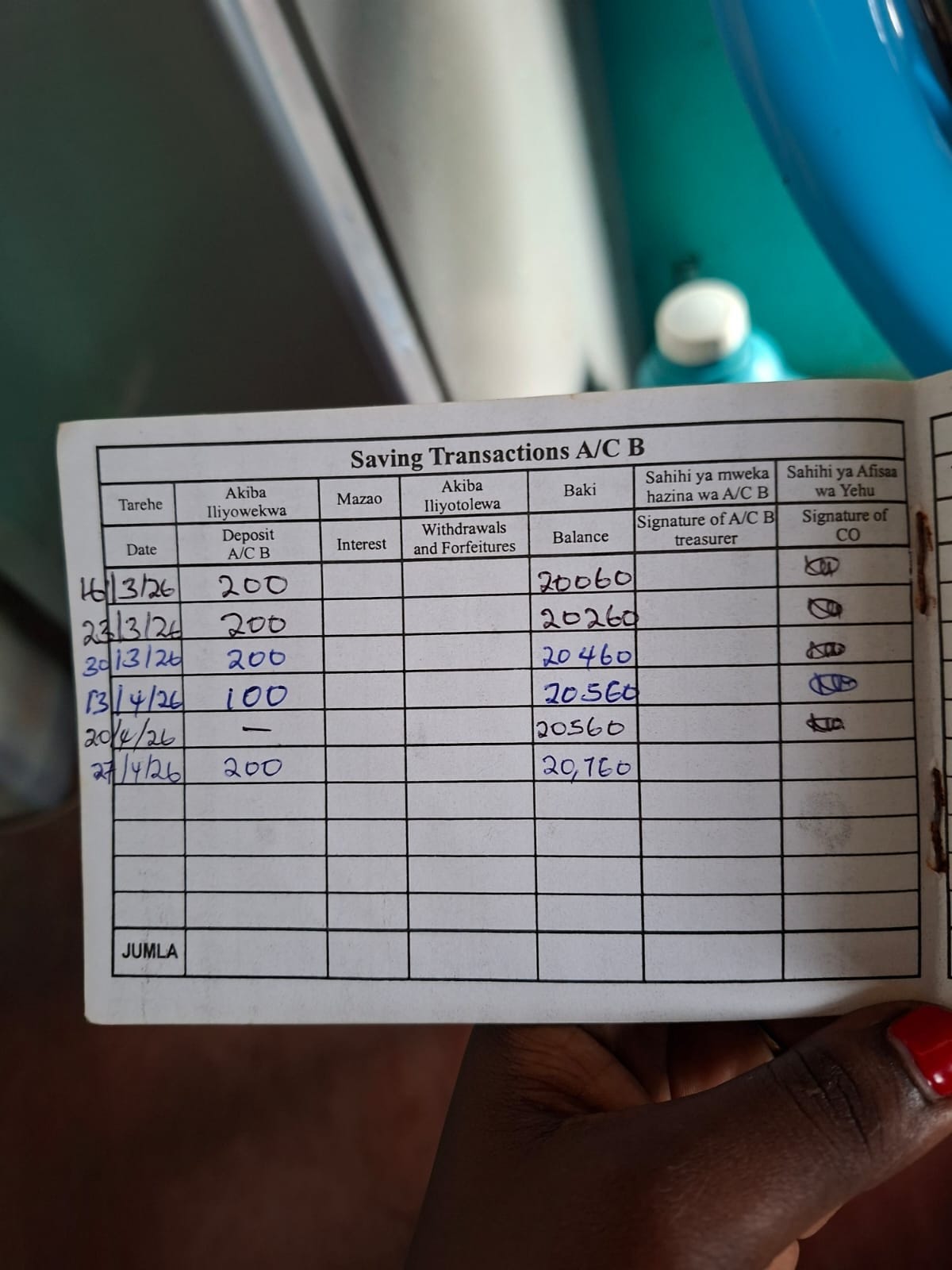

Long before any digital tools were introduced, Muungano already had strong systems in place. Members came together regularly, contributed to their shared savings, gave loans from the group fund, and recorded everything carefully in ledger books. They knew who had contributed, who had borrowed, who had repaid, and what remained.

The commitment pool is not replacing this system. It is strengthening it.

It is the familiar ledger book becoming more open, more flexible, and more useful.

A Savings System That Works More Like Mweria

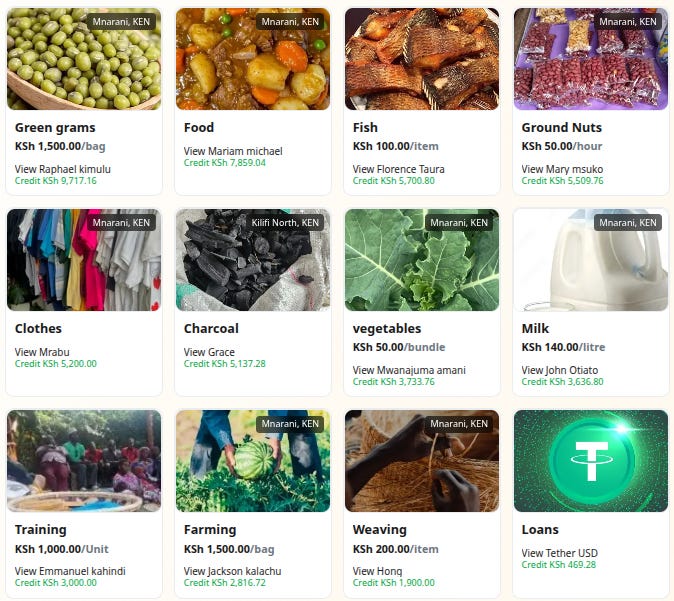

The group contributes KSh 100 weekly into a shared fund. Members can borrow from this fund interest-free and repay within one month. Traditionally, repayment was mainly understood as money returning to the group. But in real community life, people do not only hold value in cash. They also hold value in food, farming, services, labour, care, skills, and trusted relationships.

This is where the Muungano Pool becomes powerful.

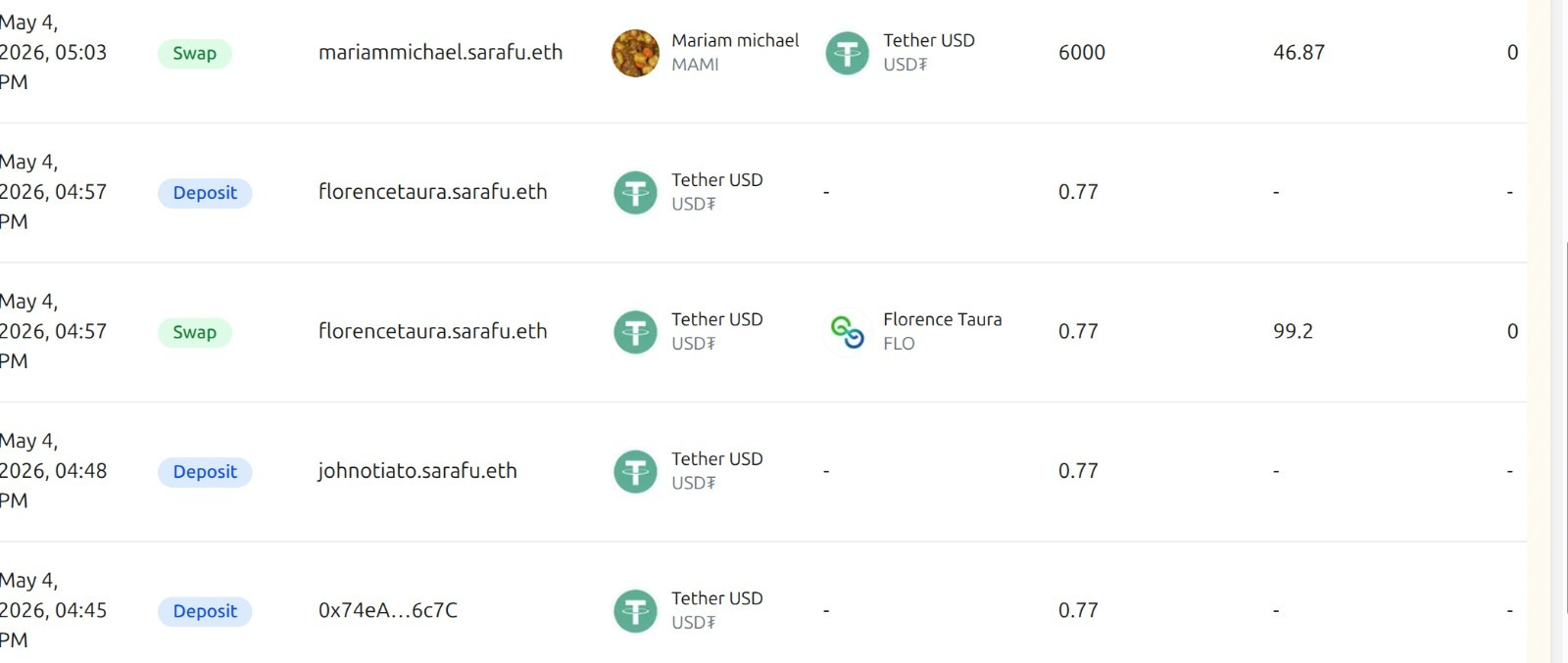

When a member pulls value from the pool, they also put in a commitment to repay. That commitment is represented as a voucher. The group holds the voucher as collateral, but it is not hidden away like a private debt record. It becomes visible inside the pool as part of a curated marketplace of community commitments.

This means repayment can happen in more than one way.

A member can repay in Kenya shillings. They can repay through goods. They can repay through services. They can also fulfill the commitment when another person takes their voucher and receives the promised value.

This makes the savings and lending system act more like Mweria, the traditional practice of mutual support where people help one another through rotating contributions, labour, and care. The pool gives Mweria a shared digital memory while keeping the heart of the practice alive.

A Community Ledger, Now Shared Digitally

At the center of this evolution is the Muungano Pool. The pool brings together cash contributions, goods, services, labour commitments, and stablecoin support into one shared system.

The group has not abandoned its physical books. Members still record contributions, loans, and balances in ledger books. At the same time, the same activity is now reflected digitally in a shared and transparent system.

This has strengthened the group in several ways. Transparency has improved because members can see transactions clearly. Accountability has increased because commitments are visible. Clarity has improved because members can understand what they owe, what they can access, and what offers are available in the pool.

It is the same trusted system, only clearer and more open.

How Debt Starts Moving

In normal lending, debt often stays fixed on one person. The borrower receives money and must return money. If they do not have cash at the right time, repayment can become stressful.

In the Muungano Pool, the person who makes a commitment remains responsible for honouring it. But the path of repayment can move through the community.

For example, a member may take an interest-free loan and place a voucher into the pool promising goods, services, or labour. Another person may need exactly what that member has promised. That second person can swap into the pool, take the voucher, and later redeem it with the original member.

In this way, the pool helps match needs and commitments. A debt is no longer only a private pressure between borrower and lender. It becomes part of a wider system of exchange, where the community can help move value toward fulfillment.

People can also contribute cash into the pool to take over someone else’s voucher. This helps reduce or clear that person’s debt while giving the person who takes the voucher access to real value in the community, such as food, services, or labour.

And when a member wants to repay directly using Kenya shillings, they can swap in KSh to pull out their own voucher. Once their voucher is removed from the pool, their loan is considered repaid.

Link: Muungano Pool

Real Support, Real Commitments

Members are already using the pool to meet important needs.

Mary Msuko received an interest-free loan to help pay her child’s school fees. She has committed to repay by the end of the month.

Rafael K. Muli, a small-scale farmer who grows green grams, also accessed support through the Muungano Pool. With an interest-free loan, he was able to acquire an additional acre of land in Kilifi County. This expansion is expected to increase his yields and improve his income.

These stories show that the pool is not only about borrowing money. It is about creating more ways for people to meet needs, repay responsibly, and keep value moving within the community.

Strengthening What Already Exists

The Muungano Pool builds on what the elders already had: trust, records, discipline, savings, mutual support, and regular meetings. With the support of Emmanuel Kahindi, the group is showing how a local savings and lending system can grow into a living marketplace of commitments.

This is not innovation from outside replacing tradition. It is tradition becoming more visible and more flexible.

From ledger books to blockchain, and from weekly contributions to shared vouchers, the core idea remains the same: people showing up for one another.

Upendo Kiriba: Basic Income That Keeps Rotating

By Njambi Njoroge

In Kiriba Village, another version of this same pattern is taking shape.

Here, the starting point is not weekly savings from elders, but pooled basic income support provided through FairSpirit Foundation in collaboration with Grassroots Economics Foundation. The first phase supported the Kiriba Chama group. The second phase extended support to Upendo Kiriba, another active community group in the same village.

With the support of George Shungu, groups in Kiriba are showing how basic income can become more than a one-time cash transfer. When placed into a commitment pool, basic income becomes a seed that can rotate through the community.

From One-Time Support to Continuous Flow

A one-time transfer can help a household solve an urgent problem. That matters. But once the money is spent, the flow can end.

A pooled basic income model works differently.

The funds enter a shared pool. Members access support based on their needs and participation. When someone takes from the pool, they also make a commitment to support the next members through cash, goods, services, or labour. Their voucher enters the pool and becomes part of the group’s marketplace.

This means the original support does not simply disappear after the first use. It becomes the beginning of a chain of commitments.

Someone may use the support to hire land for farming. Another may expand a small business. Another may repair a kitchen roof. Each person receives value, but each person also remains connected to the group through a commitment to continue the flow.

That is the regenerative difference.

The basic income is not only consumed. It is transformed into circulation.

Link: Upendo Kiriba Commitment Pool

How Members Used the Support

In this cycle, Upendo Kiriba members used the funds for practical livelihood and household needs.

Tabu Ndoro used the money to hire a shamba and begin farming.

“I used the money to hire a shamba so that I can start farming. This has given me a chance to grow my own crops and improve how I support my household. I am very grateful for this support because it came at the right time and helped me take this step.”

Karabu Kisiwa used the funds to expand a mnazi business.

“I used the funds to expand my mnazi business. I was able to increase my stock and improve my daily sales. This support has helped me strengthen my business, and I am very thankful because it is making a difference in my life.”

Agnes Joseph invested in farming by buying seeds and seedlings.

“I bought seeds and seedlings so that I can prepare for planting. Now I am ready to work on my farm. I am grateful for this support because it helped me invest directly in my farming.”

Loyce Baya used the money to buy makuti and repair her kitchen roof.

“I used the money to buy makuti to repair my kitchen roof. Now my kitchen is in a better condition and safer to use. I really appreciate this support because it helped me solve an important problem at home.”

Each story is simple and practical. Farming. Business. Shelter. Household safety. But together they show something larger. The pool allows support to respond to real needs while also asking each person to remain part of the flow.

A Marketplace of Trust

Inside the pool, commitments become visible. This matters because the group can see what is being offered, who has received support, and how value is expected to return.

The pool becomes a curated marketplace, not in the sense of an outside market where people only buy and sell, but as a community space where trusted offers can be exchanged. A voucher represents a promise. The group helps curate which promises are accepted. Members can then use those promises to access real value.

This public record supports accountability. It also supports trust. People are not only receiving assistance. They are participating in a shared system that remembers contributions, commitments, and repayment.

Two Different Seeds, One Shared Pattern

Muungano and Upendo Kiriba begin from different places.

Muungano begins with group savings. Members contribute every week, borrow from the shared fund, and use the commitment pool to create more flexible ways to repay.

Upendo Kiriba begins with basic income support from FairSpirit Foundation. The pool helps that support rotate, so one grant can continue activating farming, business, household repair, and future commitments.

In both cases, the pool changes the shape of support.

The seed may be savings.

The seed may be a grant.

The seed may be commitments of goods and services of members.

The seed may be stablecoin support from partners.

The seed may be Kenya shillings from members.

But once that value enters the pool, it can begin to move differently.

People can pull what they need while putting in what they can promise. The group holds those promises as vouchers. Others can use those vouchers. Repayment can happen through cash, goods, services, labour, or fulfillment. The system creates more paths for value to return.

That is why this is not just lending.

That is why this is not just cash allocation.

That is why this is regenerative.

Why This Matters

A normal loan asks: can this person repay money?

A commitment pool asks: what value does this person already have, what can they commit to, and how can the community help that value move?

A normal cash transfer asks: who receives support today?

A pooled basic income system asks: how can today’s support become tomorrow’s support for someone else?

These are different questions, and they lead to different systems.

In Mnarani, elders are showing how savings and lending can become more flexible, relational, and transparent. In Kiriba, community groups are showing how basic income can become a rotating source of livelihood support. In both places, the pool helps transform support into circulation.

And as value keeps moving, repayment becomes easier.

As repayment becomes easier, reciprocity continues.

As reciprocity continues, trust grows.

That is the heart of a regenerative economy: not money moving once, but commitments moving again and again through relationships that become stronger over time.

| A guest post by

|

| A guest post by

|

Great article, I like how you mention "A commitment pool gives trust a shared place to move."