Cosmo-local (credit) network: locally governed, globally connected. The term and practice were popularized by

and colleagues at the P2P Foundation- design and know-how as well a credit circulate as a commons, while production, governance, and accountability remain rooted in place.In this article, we explore how a traditional ROSCA (Rotating Savings and Credit Association or Village Savings and Loan Association or Credit Union) can evolve into a more dynamic and resilient system by integrating Commitment Pooling. By doing so, not only do the types of assets within the group diversify, but the capacity to route credit (and spread out risk) across entire networks expands dramatically. This model also organically covers many types of community-based insurance, where access to pooled resources is granted based on approved need.

Understanding the Commitment Pool Model

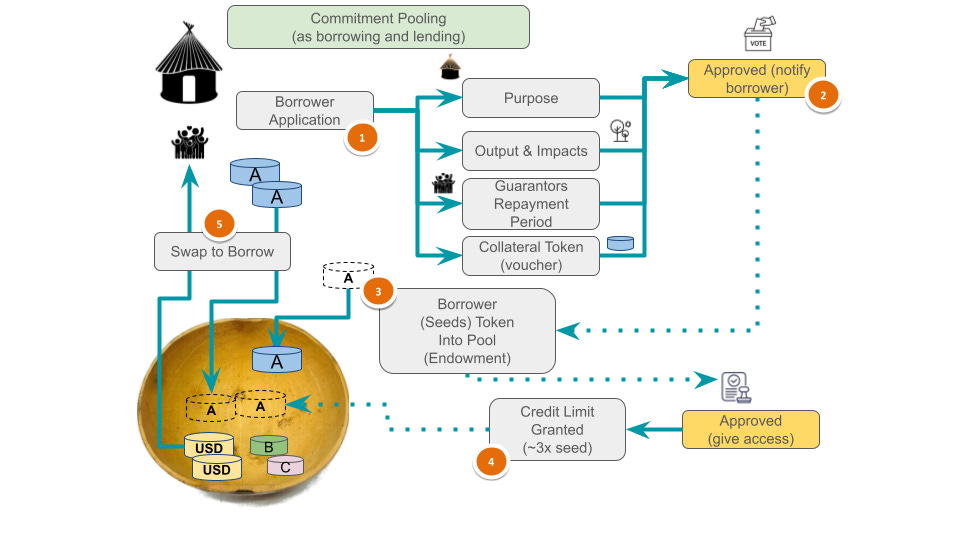

While each group decides its initial pool setup and seeded resources, we begin here with a new member. The process starts with a borrower application (1) stating purpose, expected outputs and impacts, repayment period, guarantors, and collateral—usually a digital voucher for the borrower’s own goods or services. If approved (2), the borrower seeds an initial endowment (3) of their vouchers into the shared pool. After verification, a credit limit (4) is granted—typically up to 3× the seed—and the member can swap (5) their vouchers to withdraw needed resources. The borrower’s debt equals the value of their own vouchers currently held by the pool; available credit is remaining room in the pool under their credit limit.

Note that humanitarian actors and well wishers can as well offer endowments to the pool - as a healthy form of aid.

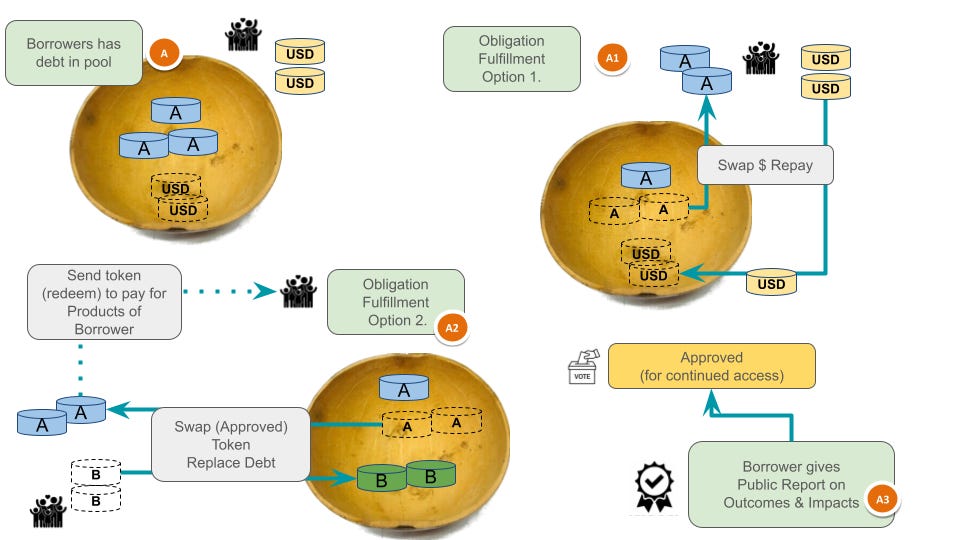

The vouchers left in the pool represent the borrower’s debt. Before the repayment date, obligations can be fulfilled in two ways:

Option A1: The borrower swaps back the same asset(s) they withdrew, removing their vouchers from the pool.

Option A2: Another member swaps approved tokens into the pool to remove the borrower’s vouchers (replacing the debt) and then redeems those vouchers directly with the borrower.

After fulfillment, the member submits an Impact Report (A3) for verification; access can be continued or paused based on performance. If obligations are not met on time, the member’s credit is suspended, guarantors are engaged, and the group may resolve the shortfall through voucher resale, routing swaps, or negotiated in-kind redemption.

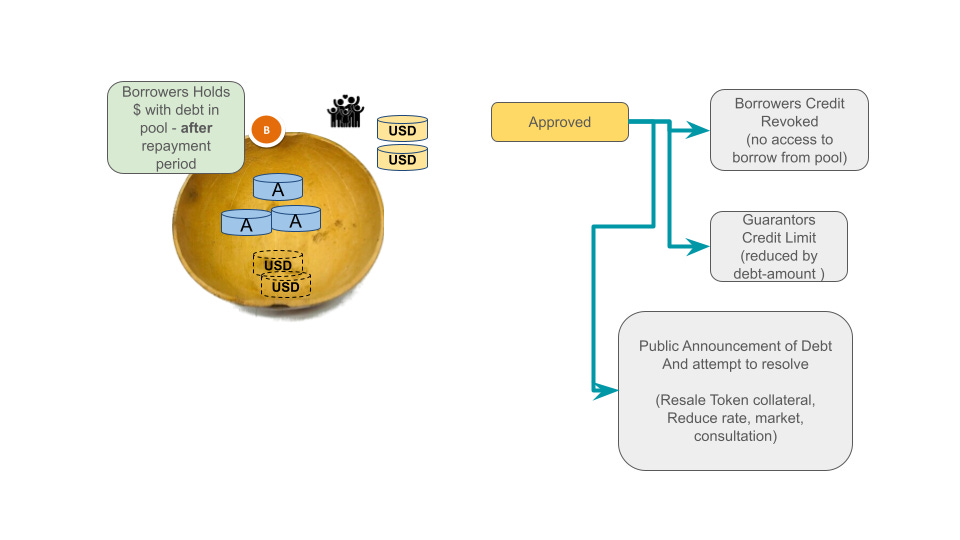

Failure to fulfill obligations results in revoked credit access and penalties to the guarantors. The community can also publicize the debt and seek to resolve it through various means, including voucher resale, negotiation, or mutual consultation.

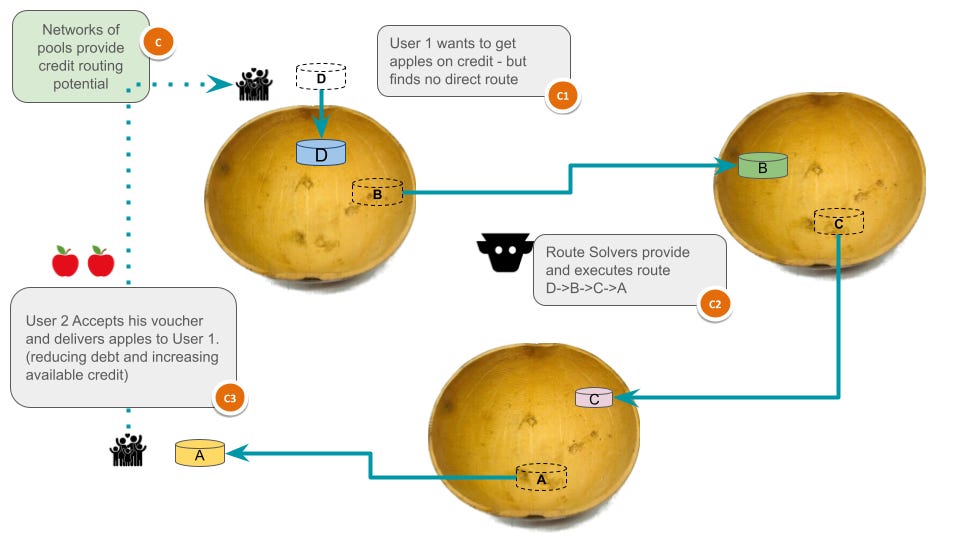

A network of pools allows credit routing across distant pools. For example, if someone needs apples but can't access them directly, a routing path (e.g., D → B → C → A) can be executed through the network to fulfill that need.

Below is a brief agenda for a typical trainings happening in Kenya:

Training Brief: Commitment Pooling for Community Lending Groups

Purpose

This brief outlines a practical, values‑aligned training that equips community champions and local groups to design, launch, and steward Commitment Pools - trust‑based systems that track promises (vouchers), route credit, and strengthen mutual aid. The approach honors Mutual-Aid traditions (Mweria, Goob) and Islamic finance principles (no interest, endowment/waqf logic) and supports transparent, accountable coordination of local resources.

This approach is cosmo-local: it links many local circles into a wider learning and routing network. Following the framing advanced by Michel Bauwens (P2P Foundation), global knowledge and coordination patterns are shared as commons, while decisions, fulfillment, and stewardship stay local.

Participants

The training is designed for Champions (Trainers of Trainers) - both experienced and new - and for chama‑style groups of roughly 10–20 members. Champions learn to facilitate, monitor, and report; groups learn to seed, use, and govern a pool.

Duration and Format

A standard delivery is one full day or two half‑days. Sessions combine plenary explanation, small‑group practice, and live simulations using paper or simple mobile tools (USSD/SMS QR Cards or Website and apps).

Preparation and Materials

Facilitators prepare a simple voucher ledger (paper or digital on sarafu.network ), name tags/aliases for USSD practice, examples of applications and reports, and tokens (beans/sticks) for games. Where available, a stablecoin wallet and a compliant on/off‑ramp may be demonstrated as optional cash‑like rails.

Training Flow

1. Introductions and Context

Facilitators welcome participants, align on expectations, and surface local experiences with mutual aid and chamas. A short overview clarifies that Commitment Pools are not markets but systems of shared promises: members seed their own vouchers, swap to (borrow) access others’ commitments, and redeem to fulfill what they owe.

2. Experiential Game: Stick/Bean “ROLA” Simulation

ROLA - Rotating Labor Association (Mweria/Goob/etc.). Participants play a short game that embodies pooling, swapping, and redeeming. Each physical card or token represents a voucher (a promise of future contribution). The game makes visible how debt accrues when one’s own voucher remains in the pool, how credit is capacity to add more, and how redemption fulfills obligations.

This is to demonstrate how vouchers can be used to keep track of commitments. Each participant gets 4 sticks or cards and they use them to appreciate people coming to help them on their farms or other activities. When they run out they need to participate in other activities to earn them back.

Their commitments here (represented as sticks or cards) as to be seen as real resources. So when we look at lending programs we can see beyond only borrowing with money and only money being collateral.

3. Commitment Pool Fundamentals

In plain language the facilitator explains: a loan equals a swap (you put your voucher in and withdraw another); debt is the value of your own vouchers currently held by the pool; redemption is when someone returns your voucher and you deliver the promised good or service. Groups practice recording swaps and redemptions and connect this to their routine weekly or monthly reporting.

4. Alignment with Islamic Finance and/or other local mutual aid traditions

This design forbids interest (riba), treats seeds as endowments (waqf-like) entrusted to the community, and shares risk through endorsement and transparency. Accountability arises from public, minimal ledgers, agreed limits, and restorative resolution.

5. Access to Credit and Lending Rules

The training demonstrates how credit can extend to individual members or nearby enterprises through group endorsement (guarantors). Applicants state purpose, expected outputs/impacts, guarantors, repayment period, and provide collateral as product/service vouchers. After a small initial endowment, members may receive a credit line up to ~3× the seed (e.g., deposit 100 units, borrow up to 300 units). If a borrower fails to redeem on time, the endorsing group’s access is paused until the obligation is resolved—creating strong incentives to back reliable commitments and to support timely fulfillment.

Including Those in Extreme Need

The pool is explicitly inclusive: people with limited capacity (elderly, disabled, single caregivers, or crisis-affected) can participate through proxy voucher issuance and guarantor support. Guarantors co-endorse applications and commit to redeem or replace unfulfilled vouchers by swapping approved tokens, ensuring access without interest or exclusion.

Example – Guarantors Backing a Highly Vulnerable Member. A member with severe mobility constraints applies for a small line of credit to cover essentials. The group seeds a modest endowment on the member’s behalf, two neighbors act as guarantors, and a nearby vendor accepts the member’s vouchers. If the member cannot fulfill on time, guarantors either redeem the vouchers in kind (e.g., delivering agreed services) or swap in their own approved tokens to clear the balance. The member receives timely support, remains included in the pool, and no interest is charged - while accountability is maintained through transparent endorsement and redemption.

6. Using the Pool with Vouchers and Optional Digital Cash

Participants practice swaps and redemptions via paper ledgers and, if available, simple mobile flows (USSD/SMS/app). An optional module introduces a stablecoin wallet for cash‑like swaps, alias‑based sending, and a compliant mobile money on‑ramp for topping up and repaying. Every loan requires a short pre‑loan plan and a post‑repayment outcomes & impact note recorded by the champion of the group.

7. Stewardship, Governance, and Safeguards

Facilitators emphasize that champions curate entries and keep only authentic, traceable commitments in the pool. Groups co‑set limits, endorsement criteria, and dispute processes. Safeguards include: simple consent for any data captured; public but minimal records; rotating review circles; and clear steps for delinquency - temporary credit suspension, guarantor engagement, and community‑led resolution (e.g., routing other approved tokens to replace debt, or redeeming the borrower’s vouchers in kind).

8. Network Effects and Routing

Participants learn that multiple pools can interoperate. If a direct swap is not possible, a route across pools can be found (e.g., D→B→C→A) so that someone who wants a product can still fulfill a borrower’s obligation by exchanging along a path. This expands liquidity and reduces bottlenecks without introducing interest or speculation.

Monitoring, Reporting, and Learning

Champions collect simple indicators: number of swaps and redemptions, fulfillment rate, average time to redemption, active commitments by type, and stories of resolved shortfalls. Short reflection circles at the end of the cycle review what worked, adjust limits, and welcome new members.

Inclusion and Accessibility

The design welcomes basic‑phone users (USSD/SMS) and low‑literacy participants (icons, color‑coding, QR Cards). Meetings are scheduled around care and prayer times, and translation is arranged as needed. No one is excluded for lack of smartphones or cash; vouchers are primary.

Expected Outcomes

Participants leave able to describe and run a commitment pool; champions can teach the ROLA simulation, create vouchers, record swaps, and steward reports; groups can apply lending rules that honor endorsement, collateral, and on‑time redemption; and local governance is strengthened through transparent limits and restorative resolution paths.

Follow‑Up Support

After training, champions receive a concise facilitation pack (ledger templates, application and report forms, endorsement checklist) and a helpline contact. A 30‑day check‑in reviews early data and, if appropriate, scales limits or links to neighboring pools to improve routing.

Core Principle: We are weaving a network of promises. Trust moves value. Every fulfilled commitment strengthens the whole.

Onward

Including Those in Extreme Need. The pool is explicitly inclusive: members with limited capacity (elderly, disabled, single caregivers, or crisis-affected) can participate through proxy voucher issuance and guarantor support. Guarantors co-endorse applications and agree to redeem or replace any unfulfilled vouchers by swapping approved tokens, ensuring access without interest or exclusion.

In places where differentiated assistance pits “visible vulnerability” against community cooperation, commitment pooling dissolves the conflict by turning mutual aid from a disqualifier into an eligibility signal. Transparent vouchers and simple ledgers make care visible and verifiable, so groups no longer need to hide their practices; endorsed credit and clear limits align incentives, while no-interest, waqf-style endowments amplify existing support rather than replace it. When obligations slip, restorative pathways - redeeming the borrower’s vouchers in kind, routing swaps across pools, and engaging guarantors - resolve shortfalls without punishment or exclusion.

In effect, this method shifts aid from scarcity triage to trust-based routing of commitments, reducing gaming and resentment, strengthening local governance, and ensuring assistance lands where people are already showing up for one another.

| A guest post by

|

This is an intriguing concept, given that you have conducted these experiments for many years. I recall the talk you gave in Osaka during Devcon about community currency five years ago (?) during Devcon, which was also fascinating. Do you think more experimentation is needed? What part of the concepts needs to be tested?

OMG thats some really fucking dumb shit there tech bro. Seriously!